and rising outdoor water (1) (1)")

How to File a Water Damage Insurance Claim in Grand Rapids: A Homeowner’s Guide

Table of Contents

Walking into your basement to find a foot of standing water or dealing with the aftermath of a sudden sewage backup is an absolute nightmare for any Grand Rapids homeowner. We know the feeling, the sinking sensation in your gut, the stress of ruined belongings, and the overwhelming fear of the costs involved. Navigating a water damage insurance claim shouldn’t add to that trauma. At RAM Restoration, we’ve helped countless neighbors in Kent County through the restoration process, and we know that the right information is the best tool for a quick recovery. This guide will walk you through exactly how to handle your insurance company and ensure your home is restored to its original state.

Does Grand Rapids homeowners insurance cover flood damage?

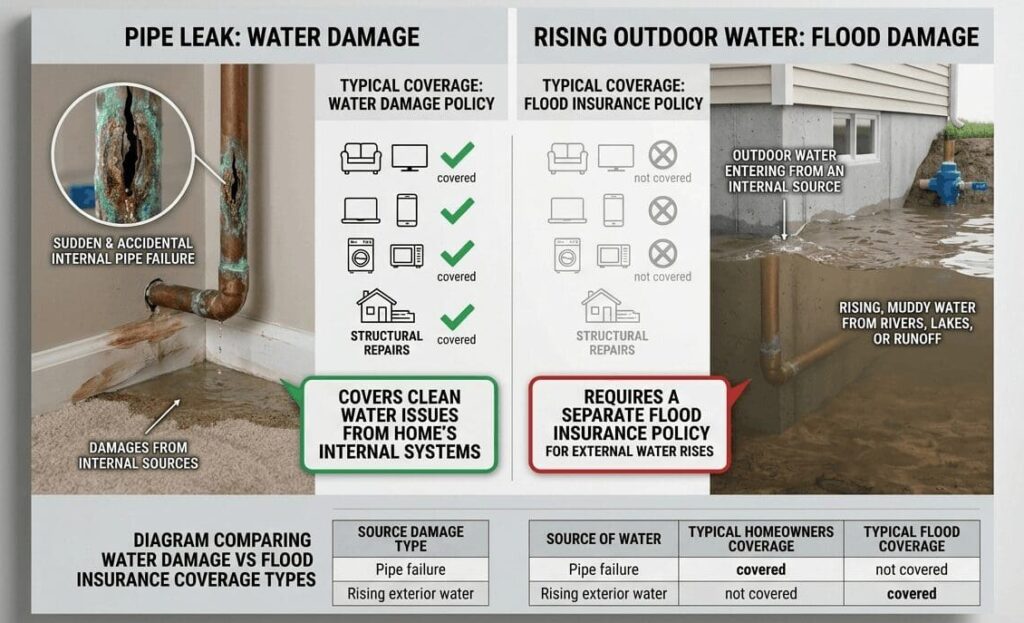

No. Standard homeowners insurance policies in Michigan generally exclude flood damage caused by rising groundwater or overflowing bodies of water like the Grand River. To be covered for such events, you must have a separate policy through the NFIP (National Flood Insurance Program) or a private flood endorsement.

What is the difference between flood vs water damage coverage?

In the insurance world, “water damage” and “flood damage” are not the same thing. Generally, standard policies from providers like State Farm or Allstate cover “sudden and accidental” water discharge, such as a burst pipe water damage event. However, if the water comes from the ground up such as during a Grand River flooding event, it is classified as a flood and requires specific flood insurance.

How to document water damage for insurance properly?

To ensure your water damage insurance claim is successful, you must act like a private investigator. Before you throw anything away or start cleaning, take high-resolution photos and videos of the standing water and all affected materials. Create a detailed inventory list of damaged items, including their approximate age and original cost. This level of detail follows IICRC documentation standards, which adjusters look for when validating the scope of the loss.

What should I expect from an insurance adjuster for water damage?

When the insurance adjuster for water damage arrives at your Grand Rapids home, their job is to determine the cause of loss and the extent of the damage. They will inspect the point of failure and look for signs of pre-existing damage or lack of maintenance. It is highly beneficial to have a professional from RAM Restoration present during this inspection to ensure the adjuster doesn’t overlook hidden moisture behind walls or under flooring that could lead to mold.

Why is a water damage claim denied in Grand Rapids?

A water damage claim denied in Grand Rapids is usually the result of gradual damage or lack of maintenance. For example, if a slow leak has been occurring behind a shower wall for six months, the insurer may argue you failed to prevent the loss. Other reasons include missing the filing deadline or the damage being specifically excluded under your policy, such as a sewer backup if you don’t have a specific Sump Pump and Sewer Backup endorsement.

Learn the critical steps in sewage backup cleanup in Grand Rapids.

5 Proven Steps to Filing Your Water Damage Insurance Claim

Learn the essential steps to successfully file a water damage insurance claim in Grand Rapids. This expert guide covers everything from initial mitigation and professional documentation to navigating policy limits and insurance billing to ensure your Kent County home is restored quickly.

3–7 Days

Step 1: Safety First and Damage Mitigation

The moment you discover damage, ensure the area is safe. Turn off electricity if water is near outlets. Your policy actually requires you to mitigate the damage, meaning you must take reasonable steps to stop further harm. This is where calling RAM Restoration immediately is vital, we provide the emergency extraction needed to satisfy your insurer’s requirements.

Step 2: Contact Your Agent Immediately

Notify your insurance carrier as soon as possible. Whether you use a local agent or a national carrier like Allstate, early notification is key. Ask for your claim number and the contact information for the adjuster assigned to your case.

Step 3: Professional Inspection and Documentation

Don’t rely solely on the insurance company’s assessment. Our team uses advanced moisture meters and thermal imaging to document the full extent of the saturation. We provide a comprehensive report that adheres to the Michigan Dept. of Insurance and Financial Services (DIFS) guidelines for consumer protection.

Step 4: Understand Your Policy Limits

Review your declarations page. You need to know your deductible amount and whether you have Actual Cash Value (depreciated) or Replacement Cost coverage. If your home was affected by local rising waters, check if your NFIP policy is active.

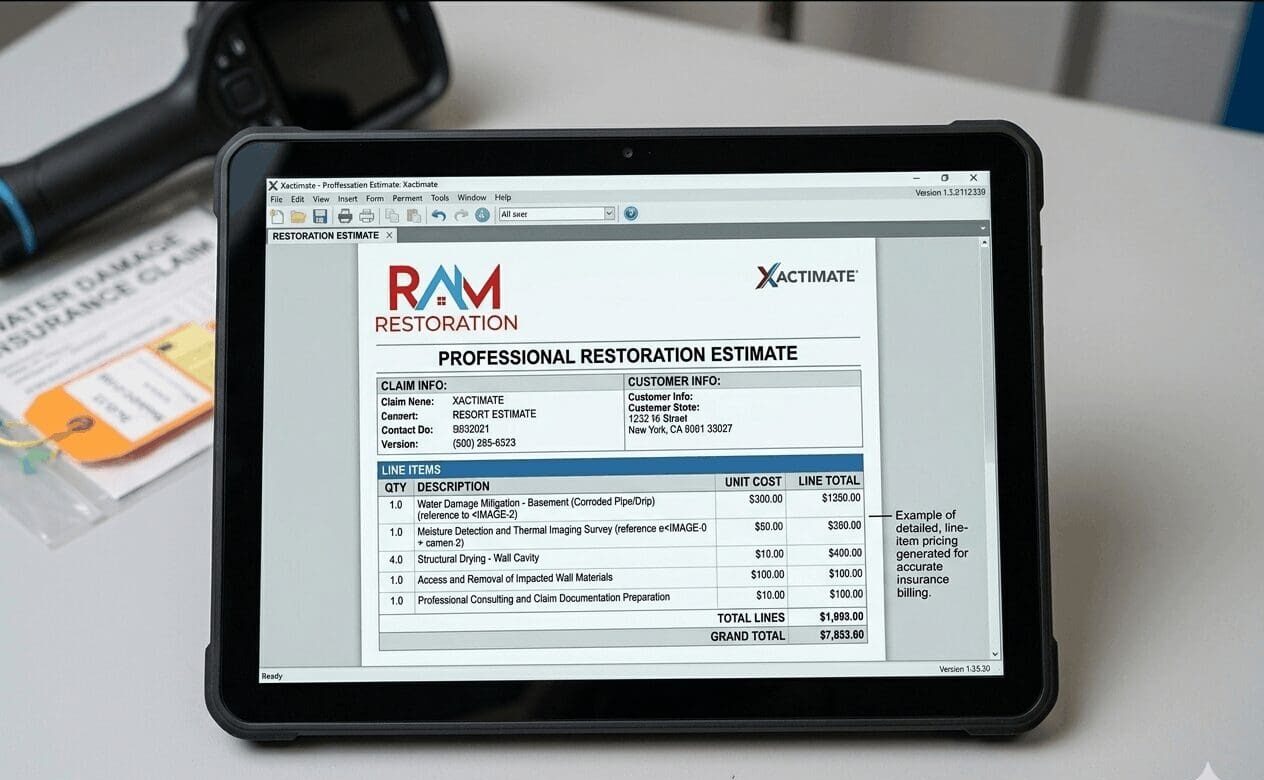

Step 5: Managing Restoration Company Insurance Billing

One of the biggest stressors for homeowners is the financial aspect. At RAM Restoration, we specialize in restoration company insurance billing. We use Xactimate, the same estimating software used by most adjusters, to ensure our pricing is transparent and aligned with industry standards. This minimizes out-of-pocket friction for you.

Why Choose RAM Restoration for Your Claim Needs?

When disaster strikes your Grand Rapids home, you need more than just a cleaning crew; you need a partner who understands the complexities of a water damage insurance claim. Serving Kent County and the surrounding communities, RAM Restoration brings years of expertise and IICRC certification to every job.

We provide:

- 24/7 Emergency Response: We are on-site fast to stop the damage.

- Expert Documentation: We provide the proof your adjuster needs to approve the claim.

- Direct Insurance Billing: We take the paperwork off your plate.

Don’t navigate the insurance maze alone. Call RAM Restoration (616) 818-1700 now for a free assessment and let us help you get your home back to normal.

FAQ: Navigating Local Insurance Challenges

Can I choose my own restoration contractor in Kent County?

Yes. As a homeowner in Michigan, you have the legal right to hire any contractor you choose. You are not required to use the preferred vendor suggested by your insurance company. Choosing a local expert like RAM Restoration ensures the contractor is looking out for your home’s best interest, not the insurance company’s bottom line.

What if the insurance check is made out to me and my mortgage company?

This is standard practice. Because the mortgage company has a financial interest in your home, they are often named on the check. You will likely need to send the check to them for an endorsement before the funds can be released to pay for repairs.

Does homeowners insurance cover mold after a water leak?

Most policies include a limited amount of coverage for mold remediation, provided the mold was a direct result of a covered sudden and accidental water peril. However, if the mold is from long-term humidity or a slow leak, it may be excluded.

Available 24/7/365 | IICRC Certified | (616) 818-1700 | Contact Us Online | Google Business Profile

{kind=link}